The legislative echoes from the early 2020s still hold considerable sway over the economy in 2026. Many taxpayers believe that the opportunity for pandemic-era financial recovery has closed for good; however, emerging developments and specific Internal Revenue Service (IRS) statutes of limitations suggest otherwise. As of March 2026, a significant amount of relief remains available and unclaimed, largely due to evolving eligibility criteria between 2020 and 2024.

For businesses, the Employee Retention Credit (ERC) continues to be a focal point, especially with increased IRS scrutiny and a processing freeze that has carried over from previous years. For individuals, unclaimed Recovery Rebate Credits and provisions from the “One, Big, Beautiful Bill” 2025 have opened new avenues for tax efficiency and retroactive adjustments.

However, timing is critical. The opportunity to amend past tax returns is not indefinite, and navigating these options requires a clear understanding of changing regulations.

Understanding the Ever-Changing ERC in 2026

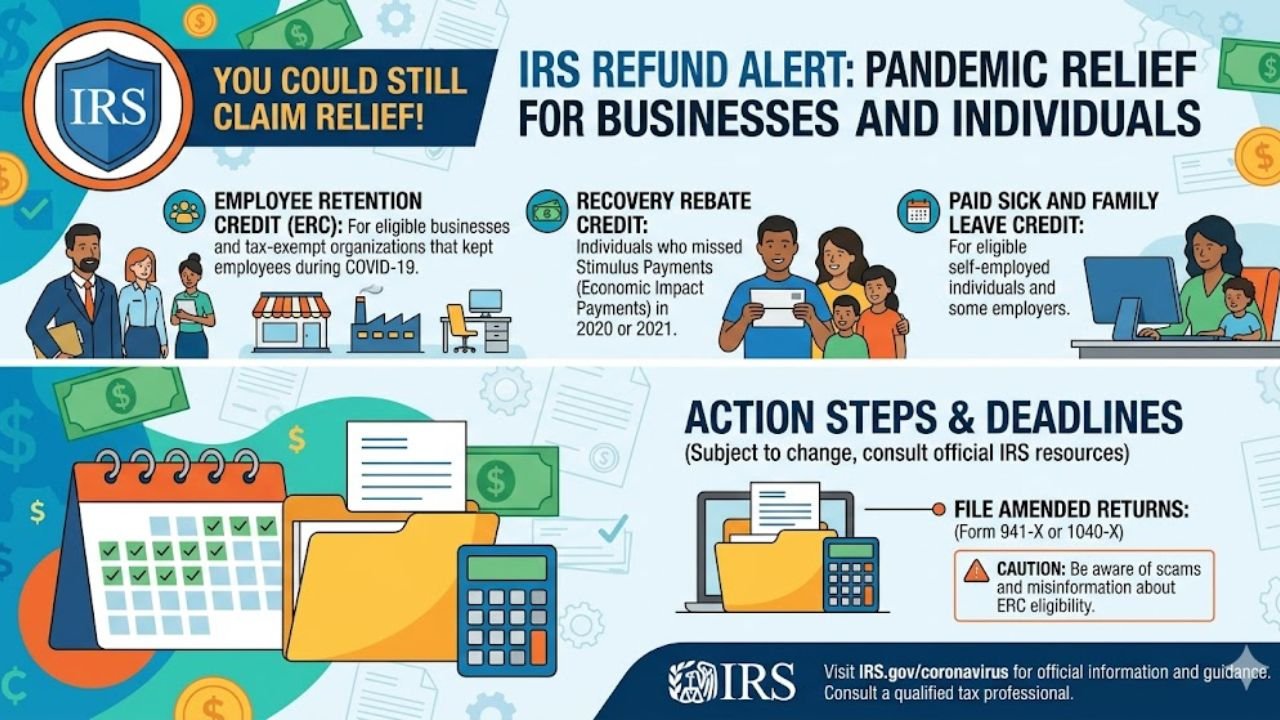

The Employee Retention Credit was designed to reward employers who retained staff during government-mandated shutdowns or periods of significant revenue decline. Although the program officially ended in late 2021, businesses still retain the legal right to claim the credit if they have not yet done so.

That said, caution is essential. The IRS has repeatedly warned against “ERC Mills,” which are deceptive promoters promising large refunds without proper qualification. Businesses must demonstrate either a full or partial suspension of operations due to government orders or a measurable decline in gross receipts compared to 2019.

In 2026, audit activity is increasing, especially for high-risk claims. Even essential businesses must maintain detailed documentation showing how their operations were impacted by restrictions. The IRS generally allows a three-year window to amend returns, meaning deadlines tied to 2021 filings are rapidly approaching.

A recent federal court case, Kwong v. United States, has introduced new interpretations of disaster-related extensions. As a result, some taxpayers may have until July 10, 2026, to file protective claims for refunds related to penalties or interest.

Comparing Pandemic Relief Programs

It is important to distinguish between the various relief programs, as eligibility and benefits differ significantly depending on whether you are a business owner, self-employed worker, or individual taxpayer.

Relief Program

Target Group

Key Eligibility Criteria

Maximum Benefit

Employee Retention Credit (ERC)

Businesses / Non-Profits

Revenue decline or government shutdown

Up to $7,000 per employee per quarter

Recovery Rebate Credit

Individuals

Missed stimulus payments

Varies by tax year (2020/2021)

Paid Sick & Family Leave

Self-employed / Small businesses

COVID-related illness or caregiving

Up to $511 per day

Section 7508A(d) Claims

All taxpayers

Federal disaster impact

Penalty and interest abatement

Protecting Your Claim from IRS Scrutiny

The IRS is now leveraging advanced AI tools to identify anomalies in relief claims for the 2026 filing season. This means that incomplete or loosely documented claims are more likely to face delays or audits.

To ensure compliance, businesses should maintain copies of government shutdown orders, detailed payroll records distinguishing qualified wages from PPP-funded wages, and comprehensive revenue documentation. Poor recordkeeping can lead to refund delays that stretch into multiple years.

For individuals, it is important to avoid conflicts between previously claimed credits and new provisions introduced in 2025 legislation, such as “no tax on tips” or “no tax on overtime.” The IRS may issue Letter 6612 requesting additional documentation, and a prompt, organized response is critical to releasing frozen refunds.

Changes in Refund Processing and Direct Deposit Requirements

The IRS has updated its refund processing systems, with a strong preference for direct deposit due to fraud concerns. Refunds tied to amended returns from 2021 or 2022 will only be processed efficiently if accurate direct deposit information is on file.

Taxpayers may receive a CP53E notice requesting updated banking details. Failure to respond can result in refund delays of six to eight weeks, after which the IRS may issue a paper check instead.

FAQs

Q1 Can you still claim the Employee Retention Credit (ERC) in 2026?

Yes, in many cases. Businesses can still claim the ERC for 2021 if they are within the three-year amendment window. This is done by filing an amended Form 941-X, provided the original return was filed within the allowable timeframe.

Q2 Is it still possible to claim missed stimulus payments?

Stimulus payments can be claimed as a Recovery Rebate Credit by amending 2020 or 2021 tax returns. While most taxpayers are past the deadline for 2020 claims, the 2021 window may still be open, especially for those with valid extensions.

Q3 What is the significance of the July 10, 2026 deadline?

This date is becoming a critical deadline for filing protective claims related to penalties and interest assessed during the pandemic. Due to recent court interpretations of disaster relief laws, some taxpayers may have been incorrectly penalized despite filing within extended deadlines.

Paradise Diving Club is a professional diving center that offers scuba diving, snorkeling, and underwater adventure experiences.