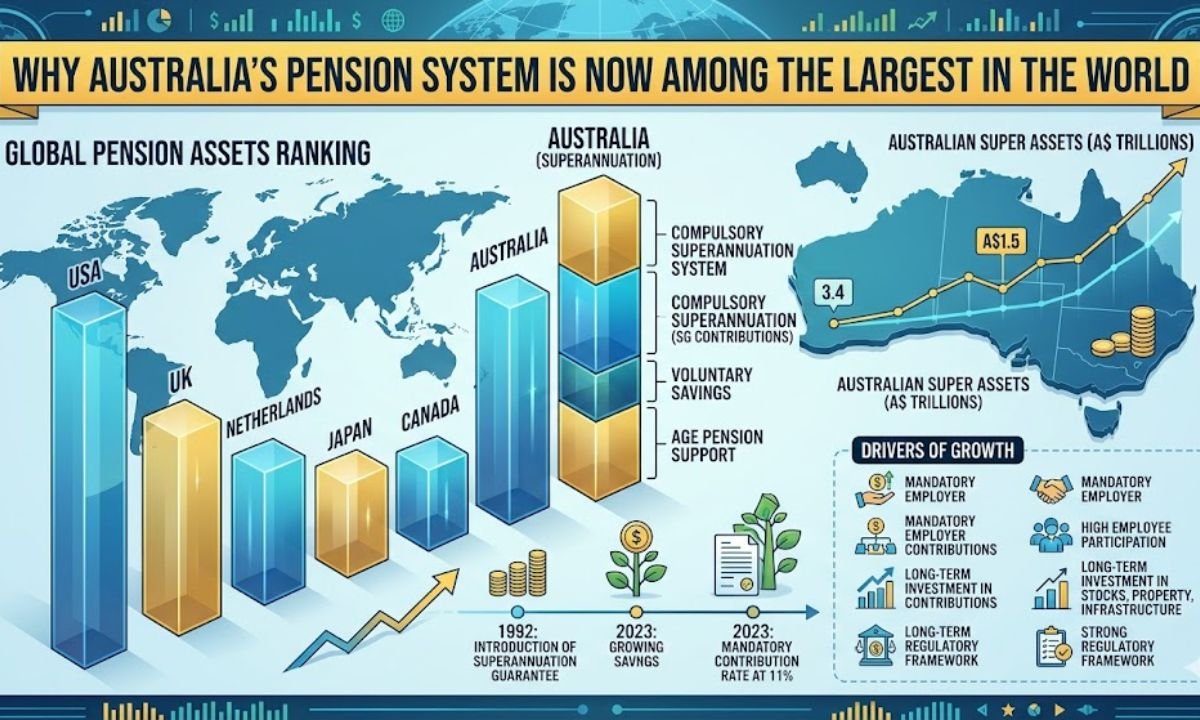

Over the last three decades, Australia’s retirement income system—commonly known as superannuation—has undergone a remarkable transformation. What began as a modest domestic policy initiative has evolved into the fourth-largest pension system in the world. According to global financial institutions, Australia is now among the top ten countries with the largest pension assets.

The system currently holds around $4.5 trillion AUD in assets and continues to grow at an impressive rate of approximately 11–12% annually. This rapid growth is largely attributed to sophisticated public policy and a structured framework designed to maintain sustainability even during economic downturns.

Rapid Growth of Australia’s Superannuation System

The modern superannuation system began gaining momentum in 1992 with the introduction of the Superannuation Guarantee (SG). Initially set at just 3% of wages, this mandatory employer contribution has steadily increased over the years and is projected to reach 12% of gross salary by 2025.

This gradual increase in mandatory contributions has been one of the main drivers behind the system’s massive expansion. As contributions grew and investment funds accumulated over time, Australia quickly rose into the ranks of the world’s largest pension markets.

The system also benefits from strong participation. Unlike voluntary retirement savings models, such as the U.S. 401(k), Australia’s compulsory framework ensures that nearly the entire workforce contributes to retirement savings.

The Power of Long-Term Investing

One of the defining features of Australia’s superannuation system is its preservation rule. Employees cannot access their superannuation savings until they reach a specific retirement age. This restriction allows investments to compound over several decades.

Long investment horizons also allow superannuation fund managers to allocate capital to illiquid assets such as infrastructure, airports, toll roads, and renewable energy projects. These assets often deliver higher long-term returns than traditional stocks and bonds.

As a result, the system benefits from both steady inflows of contributions and strong investment performance.

A Fully Funded System

Australia’s pension model stands apart from many Western retirement systems because it is largely fully funded. In many countries, pensions operate on a pay-as-you-go model, where taxes collected from current workers are used to pay retirees.

Australia’s approach is different. Most retirement income comes from privately invested savings accumulated during a worker’s career. This structure significantly reduces pressure on government finances and lowers long-term public pension liabilities.

Superannuation by the Numbers

- Total Assets Under Management (2026): $4.5 Trillion AUD

- Mandatory Employer Contribution: 12% of gross salary

- Projected Assets by 2040: $11 Trillion AUD

- Global Ranking: 4th largest pension system

- Annual Growth Rate: Approximately 11–12%

By 2026, the total value of Australia’s superannuation assets is expected to exceed the country’s annual Gross Domestic Product (GDP). Only a small number of nations have achieved this milestone.

The Three-Pillar Retirement System

The success of Australia’s retirement framework is built on a three-pillar structure that ensures long-term financial security.

1. Age Pension

The first pillar is the Age Pension, a government-funded safety net designed to prevent poverty among the elderly. This benefit is means-tested, ensuring that assistance is targeted toward those who need it most.

2. Compulsory Superannuation

The second pillar is mandatory superannuation contributions. This pillar acts as the primary wealth-building mechanism, allowing workers to accumulate retirement savings through employer contributions and investment growth.

3. Voluntary Private Savings

The third pillar consists of voluntary savings, which may include home ownership, private investments, or additional retirement savings plans.

Together, these three pillars create a balanced retirement income system that reduces reliance on taxpayer-funded benefits.

Impact on the Australian Economy

The superannuation system plays a major role in Australia’s broader economy. As retirement savings grow, more individuals become financially independent in retirement. This reduces pressure on government budgets and allows public funds to be directed toward other priorities such as healthcare, education, and infrastructure.

Additionally, large Australian super funds are now major global investors. Many funds have established offices in financial hubs such as London, New York, and Singapore to manage international investments.

This global investment strategy allows Australia to secure high-quality assets worldwide while strengthening its influence in international financial markets.

Future Challenges

Despite its success, the superannuation system faces several challenges. Australia’s population is aging rapidly, and more than 2.5 million Australians are expected to retire within the next decade.

This shift means the system must transition from focusing on wealth accumulation to managing the retirement drawdown phase. Policymakers and financial institutions are now developing new retirement income products designed to ensure retirees do not outlive their savings.

Balancing longevity risk, investment performance, and sustainable withdrawals will be critical in the coming years.

Why Australia’s Pension System Is a Global Benchmark

Australia’s superannuation framework is widely regarded as one of the most successful retirement systems in the world. Its strengths include mandatory participation, strong regulatory oversight, diversified global investments, and a balanced three-pillar structure.

Even as new challenges emerge, the system continues to demonstrate how consistent policy planning and long-term investment strategies can build a sustainable retirement model.

FAQs

Q1 What is Australia’s superannuation contribution rate?

For the 2025–2026 financial year, the Superannuation Guarantee (SG) rate is 12% of an employee’s ordinary time earnings.

Q2 Can I access my superannuation before retirement?

Superannuation savings are generally preserved until an individual reaches their preservation age, which typically falls between 55 and 60 years old, depending on the year of birth and meeting a condition of release.

Q3 What makes Australia’s pension system unique?

Australia’s system stands out because it is compulsory, largely privately funded, and built around long-term investment growth. Unlike many global pension systems, it relies less on government tax revenue and more on accumulated private savings.